Your credit score is a single three-digit number. It's a shortcut that lenders use to decide whether to lend to you. It can also decide what interest rate you're offered, whether you can rent an apartment, or whether you can sign up for a phone contract.

Most US scores run from 300 to 850. A score of 670 or above is usually called "good." If you've been turned down for credit, it's almost always because your score is below the lender's cut-off.

So what's actually behind the number? This article walks through the five things that shape your credit score. It explains what you can do to improve it over time. And it shares how we look at creditworthiness at Together Loans — because we think a credit score is only half the story.

The five things that shape your credit score

The most common scoring model in the US is FICO. It builds your score from five categories. Here they are in order of how much they matter.

1. Payment history (35%)

This is the biggest one. It tracks whether you've paid past credit accounts on time.

Late payments, missed payments, collections, bankruptcies, and foreclosures all hurt this category. A single payment that's 30 days late can drop your score by 50 to 100 points. It can stay on your credit report for up to seven years.

The fix is simple but strict. Pay every bill on or before its due date. Every month. Without fail.

2. How much credit you're using (30%)

This is sometimes called credit utilization. It's the percentage of your available credit that you're currently using.

Say you have a credit card with a $1,000 limit and a $700 balance. You're at 70% utilization. That's high enough to actively hurt your score.

The general rule is to stay below 30%. Below 10% is even better. One thing to know: this is measured on the day your statement closes, not on the day you pay your bill. Paying down balances before the statement date is what helps.

3. How long you've had credit (15%)

The older your oldest account, the better. Your average account age also matters.

This is one reason you usually shouldn't close your oldest credit card, even if you're not using it. Closing it shortens your average account age. That can drop your score.

4. The mix of credit you have (10%)

Lenders like to see that you can handle different types of credit. A credit card AND an installment loan (like a personal loan or auto loan) is better than just one type.

You don't need to take on debt you don't need just to improve your mix. But if you only have one type of account, adding a different type over time gives your score a small boost.

5. New credit (10%)

Every time you apply for new credit, the lender does a "hard inquiry" on your credit report. That knocks a few points off your score for up to 12 months.

Multiple inquiries in a short window look like financial stress. It's best to space out applications.

Checking your own credit is different. That's called a "soft inquiry." It doesn't affect your score at all.

What doesn't affect your credit score

A lot of things you might think matter don't matter at all. Your credit score is NOT affected by:

- Your income. Lenders may check it to see if you can afford a loan, but it isn't part of the score.

- Your savings or bank balance. Not on your credit report.

- Your employment history. Some reports show your employer, but it doesn't affect the score.

- Your age, marital status, race, religion, or nationality. Federal law bans any of these from being used in credit decisions.

- Checking your own credit. A free score check from Experian, Equifax, or TransUnion doesn't lower your score.

- Using a debit card. Debit cards aren't credit, so they don't show up on your credit report at all.

How to improve a bad credit score

If your score is below 670, here's the realistic plan for moving it up over the next 12 to 18 months. None of this happens overnight. But all of it works.

Pay every bill on time, automatically

Set up autopay on every credit account. Pay at least the minimum, every month, without thinking about it.

This single change covers 35% of your score. After 12 months of perfect payments, you'll see real improvement.

Bring your credit card balances down

Try to get every card below 30% of its limit. Then below 10%.

If you can't pay them all down at once, focus on the cards closest to their limits first. Those are doing the most damage.

Don't close old credit cards

Even if you're not using them, leave them open. They help you in two ways. They keep your average account age up. And they add to your total available credit, which lowers your utilization.

Use a credit-builder loan

A credit-builder loan is a small loan (usually $300 to $1,000). The lender holds the money in a savings account while you make payments. When you finish paying, you get the money back. Plus you've built 12 months of on-time payment history.

Become an authorized user on someone else's card

If a family member with strong credit adds you as an authorized user on their credit card, their history starts showing up on your credit report. You don't even need to use the card.

Just make sure the primary cardholder has a long history and low utilization. Otherwise it can backfire.

Check your credit report for errors

Credit reports often contain mistakes. Wrong balances. Accounts that aren't yours. Payments marked late that were actually on time.

You can pull free reports from all three bureaus at annualcreditreport.com. If you find a mistake, dispute it with the bureau. They're legally required to investigate within 30 days.

Space out new applications

Don't apply for new credit unless you actually need it. Try to avoid multiple applications within a six-month window.

The one exception: "rate shopping" for a single loan (mortgage, auto, personal). Multiple inquiries within a 14-day window usually count as one.

What if your credit is too damaged to qualify anywhere?

The honest answer is that for some people, the plan above takes too long. If you have a real financial need today and your credit is well below 600, you have a smaller set of options. But not zero.

Cosigner loans exist for exactly this situation. A cosigner is a friend or family member with stronger credit who applies alongside you. The lender looks at both of you together. We've written a full guide on how cosigner loans work.

Cosigner loans are one of the few ways to get affordable credit AND rebuild your score at the same time. On-time payments are reported to the credit bureaus in your name. Over the life of the loan, your score usually improves enough to qualify for credit on your own afterward.

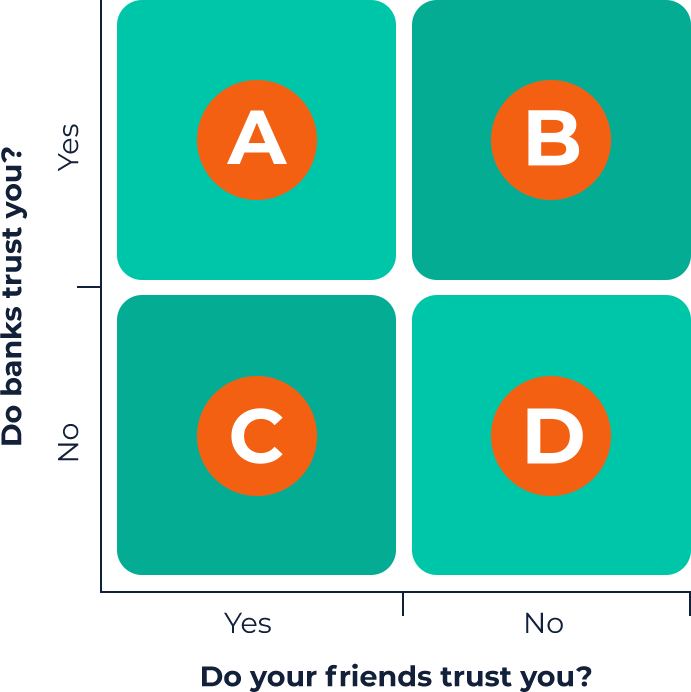

How we look at creditworthiness

Most lenders treat your credit score as the whole story. We don't. We think it tells only half of one.

We've built Together Loans around two simple questions. Every loan we write has to clear both of them.

1. Can you comfortably afford the monthly payment?

We sit down with your budget. Income. Fixed costs. Existing debt. Everyday spending. We only approve a loan if the monthly payment fits your budget with room to spare.

A payment that only works in a perfect month doesn't really work. And we'll say no.

2. Is there someone who knows you well enough to cosign?

If a friend or family member is willing to put their name on the loan with you, that's a stronger signal than any algorithm can produce. Cosigners have been used as a measure of trust for hundreds of years. Long before credit bureaus existed.

We think they're still the most accurate measure of trust we have.

Loans are paid back over 24 to 60 months. Most customers choose a 36-month term. It gives them a manageable monthly payment.

We're not the cheapest lender for someone with great credit. But for someone with bad credit and a trusted cosigner, we're a lot cheaper than the alternatives. Here's why payday loans are bad for you if that's what you're weighing us against.

If you have bad credit, can comfortably afford a loan, and have a trusted cosigner, you're exactly who we built Together Loans for. If your friends and family don't trust you with money right now, listen to them. They know you best. Borrowing is probably not the right next step.

The bottom line

Your credit score is shaped by five things. Payment history. How much credit you're using. How long you've had credit. The mix of credit you have. And new credit. Payment history and credit use together make up 65% of your score. Those are the two places to start.

If you're trying to rebuild from a low score, give it 12 to 18 months of consistent good habits. If you can't wait that long, a cosigner loan is one of the few ways to access affordable credit while rebuilding your score at the same time.

If that sounds like it could fit your situation, read our step-by-step guide on how to apply for one.